SPRING STATEMENT 2022

Spring loaded: crisis solutions or half-measures?

INTRODUCTION

Amid rising pressure to bring in significant relief measures to combat the current international emergency, Chancellor Rishi Sunak implied ahead of time that he could only do so much. Speaking at the weekend, he acknowledged concerns about price hikes and inflation, vowing to stand by people in the same way he’s “done over the past couple of years”. But, in the same breath, the Chancellor warned that the Government couldn’t “completely protect people against some of the difficult times ahead”.

After all, this year’s Spring Statement was only ever intended to be an economic update, released alongside the new Office for Budget Responsibility (OBR) forecast.

Now, against the backdrop of the most turbulent period in recent European history, a soaring cost of living crisis with inflation hitting a 30 year high, and on the second anniversary of the UK’s first lockdown, we’ve received slightly more than a brief update.

To begin with, Sunak emphasised that the “measures taken to sanction Putin’s regime are not cost-free for those of us at home” and that the OBR had reported “unusually high levels of uncertainty” about the future of the UK’s economy. He went on to announce three immediate measures designed to “help people right now”, including cutting fuel duty, scrapping VAT on energy-efficient home improvements, and doubling the household support fund. “Is that it?” cried one vocal member of Parliament during the speech. But there was more.

While hopes of a significant rescue package – like we saw during the height of Covid – may have been somewhat dashed, the Chancellor did have a few more announcements up his sleeve.

These included raising the National Insurance contributions (NICs) threshold, increasing the employment allowance, and, perhaps most notably, cutting the basic rate of income tax to 19% from 2024. But will it be enough to help households and businesses across the UK meet their skyrocketing costs? Here’s how the Chancellor’s Spring Statement might impact you.

ECONOMIC OUTLOOK

Two years to the day after the commencement of the first UK lockdown in response to the surge of COVID-19 cases throughout the country, Chancellor Rishi Sunak delivered his Spring Statement to Parliament. While the Government has essentially declared victory over the pandemic, the public finances still don’t appear all that positive – even when you keep in mind that 2020 marked the largest annual fall in GDP recorded in the UK in 300 years (9.9%).

For instance, on the morning of the Chancellor’s speech, the Office for National Statistics published its latest inflation estimate for February 2022 – 6.2% – caused by surging fuel and energy prices, exacerbated by the war in Ukraine. Sunak kicked off his speech with a summary of an economic forecast from the OBR, which is required to publish such reports twice a year.

The forecast suggests the UK will not experience as large a period of growth as previously predicted, as the OBR downgraded its GDP forecast for 2022 to 3.8% from the 6% it predicted in October 2021. It’s a far cry from its prediction in March last year that we’d see 7.3% growth in 2022, but global supply chain issues, a cost of living crisis and sanctions against Russia have hampered a similar recovery rate.

GDP will then grow by 1.8% in 2023, and 2.1%, 1.8% and 1.7% in the following three years, according to the OBR. However, it has also revised down its unemployment expectations, estimating unemployment for Q1 2022 to be 3.9%, which is 1.1 percentage points lower than expected. It added that, given the current combination of record-high vacancies and low redundancies, the slowdown in GDP growth may only cause unemployment to rise “very slightly”.

The Consumer Price Index (CPI) for inflation, meanwhile, is now expected to peak at 8.7% in Q4 2022, which would be the highest inflation rate since the 1979 oil shock. That’s double what the OBR predicted in October 2021 and was worked out with a set of market assumptions taken over the first week of the invasion of Ukraine.

With most working age benefits and state pensions due to rise by 3.1% in April 2022, the OBR also said nominal wages will not rise fast enough to prevent a “significant fall in real incomes”. However, after the peak at the end of this year, inflation will fall closer to the Bank of England’s target of 2%, at 1.5% by the end of 2023, the OBR said.

Public sector net debt, including that from the Bank of England, will equate to 95.5% of national GDP in the 2022/23 financial year, compared to 95.6% and 94% in the past two years. It will then decrease to 94.1% in 2023/24 and 91.2% in 2024/25, and 85.8% and 83.1% in the two financial years thereafter.

“It’s hard to overstate the scale of the cost of living crisis coming... But while our household finances are being hammered, the public finances have actually improved.”

Torsten Bell, chief executive of the Resolution Foundation

HEADLINE ANNOUNCEMENTS

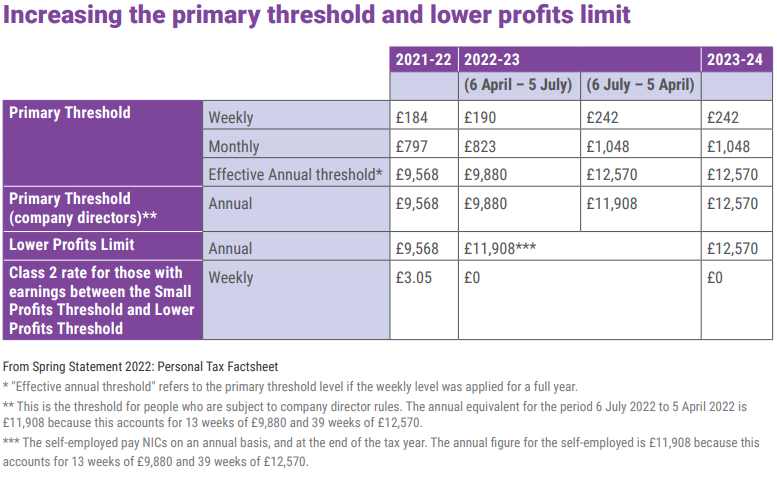

NICs threshold increase

Despite confirming that the 1.25% increase to NICs will go ahead as planned in April, the Chancellor also announced that the threshold at which people have to start paying NICs will rise by £3,000 from the 2021/22 level.

The new NICs threshold will be £12,570 and will come into effect from July, bringing the NICs and income tax threshold in line.

The Chancellor referred to this as a £6bn personal tax cut for 30 million people across the UK, worth over £330 a year for an employee, pointing to it as the “largest increase in a basic rate threshold ever, and the single largest personal tax cut in a decade.”

There are also changes to the threshold levels for NICs that self-employed people will have to pay (see table). As the changes do not take effect until 6 July in the 2022/23 tax year, an apportioned annual threshold has been calculated so that the benefit received by the self-employed is in line with employees. By 2023/24, the threshold at which employed and self-employed people start paying NICs and income tax will be aligned at £12,570.

Income tax to 19% from 2024

In the biggest surprise announcement of the day, the Chancellor announced that the basic rate of income tax will be slashed from 20% to 19% as of 2024. While heralding the move as a “tax cut for workers, pensioners, and savers”, he emphasised the fact that this will also represent the first time in 16 years that the basic rate has been cut.

Under the new basic rate, the average taxpayer will be £175 a year better off before the end of this parliament, according to the Chancellor’s tax plan, representing a £5bn total tax cut overall. The logic and tangible impact of cutting income tax, however, while continuing to raise the rate of NICs as planned, is already being questioned by some.

Fuel Duty Cut

After much speculation in recent days over whether or not the Chancellor would cut fuel duty in an attempt to combat the astronomical increase in the cost of both petrol and diesel, Sunak announced his intention to cut fuel by “not 1, not 2, but by 5p per litre”. The fuel duty cut, which applies to both petrol and diesel fuels, will knock about £3.30 off the cost of filling a typical 55-litre family car, according to the RAC.

The new duty will come into effect from 6pm on Wednesday 23 March. But, while that may be seen as a marginal gain by motorists across the UK, the OBR commented: “Higher global oil prices have already raised fuel prices, which contribute almost 0.9 percentage points to inflation in the second quarter of 2022, even after incorporating the impact of the cut in fuel duty announced in the Spring Statement”.

VAT on energy-efficient home improvements

One way households can keep their energy usage, and therefore their energy bills, down is to put in place energy-saving installments, like solar panels, heat pumps or insulation. In 2019, the scope of the VAT reduced rate for energy saving materials (5%) was restricted to comply with EU law as the UK rules were found to go beyond what was permitted.

For the next five years, however, as the Chancellor set out in the Spring Statement, homeowners installing such materials will pay no VAT at all. He added that the Government would overturn the EU’s decision to take water and wind turbines out of the scope for reduced VAT so that they will also benefit from no VAT.

Employment allowance increase

Finally, the Government is expanding support to small businesses by increasing the employment allowance from £4,000 to £5,000 per year, which will save employers an extra £1,000 in NICs. The £1,000 increase allows employers to save more and will benefit around 495,000 businesses, including 50,000 that will be taken out of paying NICs and the health and social care levy entirely.

In total, the Government expects 670,000 businesses to pay no NICs and the health and social care levy because of the employment allowance. In April 2020, the Government increased the employment allowance from £3,000 to £4,000.

UPCOMING CHANGES

As part of the Chancellor’s speech, Sunak announced several reforms and measures coming in the near future, with details of the changes we can expect to be revealed in the Autumn Budget.

Business investment tax reform

In light of economic pressures on businesses, and with the current super deduction due to end in April 2023, the Government is looking at potential tax reforms to encourage business investment. Any changes will be announced in the Autumn Budget 2022 following consultation with businesses, but the main options under consideration are:

increase the annual investment allowance permanently, for example to £500,000

increase writing down allowances for main and special rate assets from 18% to 20%, and from 6% to 8%

introduce a first-year allowance of, for example, a deduction of 40% and 13% in the first year of expenditure, with standard writing down rates applying after that

introduce an additional first-year allowance of 20% in the first year, on top of standard writingdown allowances on 100% of the initial cost over subsequent years.

introduce full expensing, allowing businesses to write off the costs of qualifying investment in one go.

R&D tax relief

Following a paper published in autumn 2021, the Government has confirmed its plans to reform R&D tax relief. From April 2023, all cloud computing costs associated with R&D, including storage, will qualify for relief.

The relief has also been focused on work carried out in the UK, although expenditure on overseas R&D activities can still qualify as long as there are:

material factors such as geography, environment, population or other conditions that are needed for the research and not present in the UK

regulatory or other legal requirements that mean activities must take place outside of the UK.

The definition of R&D for the purposes of tax relief will also be expanded, as pure mathematics will be included as a qualifying cost.

Training and the apprenticeship levy

In his speech, the Chancellor noted the need for improvements to adult technical skills, as UK employers spend “just half the European average on training their employees”. The Government said it “recognises that employers have frustrations” with the current apprenticeship levy system, and is looking at how “more flexible apprenticeship training models can be supported”. It will also consider whether further intervention is needed to encourage employers to offer training, including assessing the current tax system and the apprenticeship levy.

Changes already confirmed

The Finance Act 2022 received royal assent in February, which means a series of changes were already confirmed ahead of the Spring Statement, and are due to take place from April 2022. These include the 1.25% increase to both NICs and dividends tax in 2022/23, and the freezing of personal tax thresholds up until 2025/26. An extension to Making Tax Digital for VAT also means from April 2022, the digital tax scheme will become a requirement for all VAT-registered businesses not already required to operate MTD.

Important information

The way in which tax charges (or tax relief, as appropriate) are applied depends upon individual circumstances and may be subject to change in the future. The information in this report is based upon our understanding of the Chancellor’s 2022 Spring Statement, in respect of which specific implementation details may change when the final legislation and supporting documentation are published.

This document is solely for information purposes and nothing in this document is intended to constitute advice or a recommendation. You should not make any investment decisions based upon its content.

Whilst considerable care has been taken to ensure that the information contained within this document is accurate and up-to-date, no warranty is given as to the accuracy or completeness of any information.