Autumn Statement: ECONOMIC OUTLOOK

OBR DOWNGRADES THE ECONOMY’S GROWTH FOR THE NEXT TWO YEARS

Whilst Jeremy Hunt may have counted up no fewer than 110 measures to “help the British economy” in his Autumn Statement, the Office of Budget Responsibility (OBR) has downgraded its economic growth forecast for 2024 and 2025 from its previous expectations in the spring.

The objective of the OBR’s economic report is to summarise the UK economy, taking into account the changes made to national spending and the tax system in the accompanying Autumn Statement.

In its latest report, the OBR said that the economy has proved more resilient to the shocks of the pandemic and energy crisis than it had anticipated. However, it also added that inflation has also been more persistent and interest rates higher than it expected back in March. Overall, the economy will grow by 0.6% this year. Back in March 2023, the OBR predicted that the economy would shrink by 0.2% this year.

The OBR then expects the economy to grow by 0.7% in 2024. For 2025, GDP is forecast to rise by 1.4%, 1.9% in 2026, 2.0% in 2027, and 1.7% in 2028.

When the Spring Budget was announced, the OBR had said a return to growth was expected at a stronger 1.8% in 2024 and 2.5% in 2025, meaning the expected growth for the next two years has

been downgraded.

INFLATION AND LIVING STANDARDS

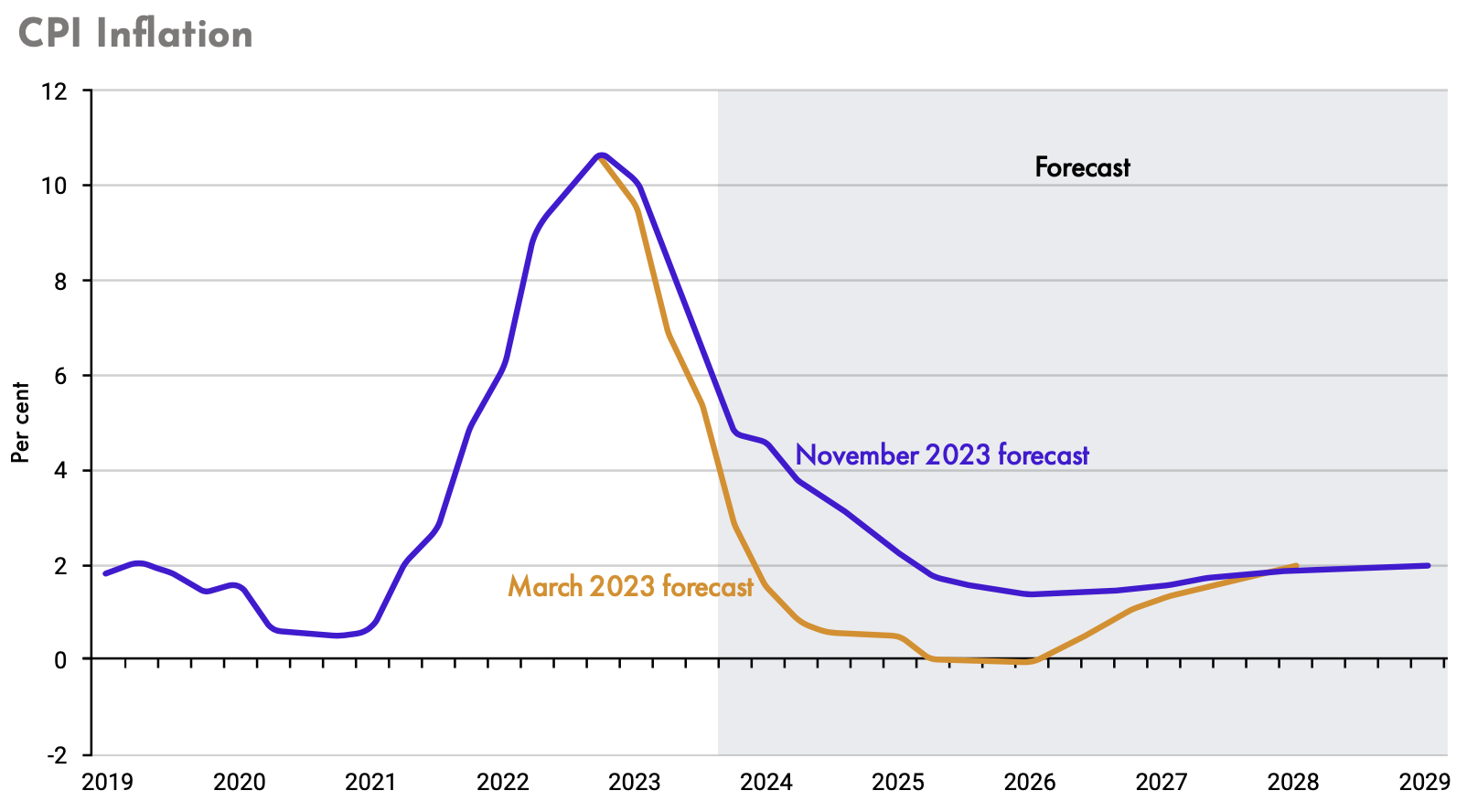

Last week the Office for National Statistics (ONS) confirmed that the rate of inflation has declined to 4.6%. The annual rate slowed in October from the 6.7% reported in September, largely due to the lower energy price cap imposed on households at the start of October.

“The easing in the annual inflation rates principally reflected negative contributions from three divisions, with large downward effects from housing and household services, food and non-alcoholic beverages, and restaurants and hotels,” the ONS said.

The lower consumer prices index (CPI) inflation figure means the Prime Minister’s pledge to halve the rate of inflation this year is currently met.

Inflation peaked at 11.1% in October last year and whilst better than it was - it has yet to return to what the Bank of England (BoE) calls “normal levels” of around 2%. It says it expects inflation to continue to slow and reach 2% by the end of 2025.

Living standards, as measured by real household disposable income (RHDI) per person, are forecast to be 3.5% lower in 2024-25 than their pre-pandemic levels. While this is half the peak-to-trough fall the OBR expected in March, it still represents the largest reduction in real living standards since records began in the 1950s.

RHDI per person recovers its pre-pandemic level in 2027-28 and the OBR estimates that the reduction in the rate of NICs announced in the Autumn Statement will boost real household incomes by around 0.5% at the end of the forecast.

Unemployment is now expected to peak at 4.6% in the second quarter of 2025 as GDP growth slows and spare capacity opens up. The ONS said that while labour market participation was falling, labour demand has weakened, with vacancies falling from a peak of 1.3m in May 2022 to around 960,000 in October 2023.

PUBLIC FINANCES

On public debt, Hunt stuck to the two new fiscal rules he introduced a year ago, dictating that underlying debt must fall as a percentage of GDP in five years’ time.

The OBR forecasts that underlying debt will be 91.6% of GDP next year, 92.7% in 2024-25, peaking at 93.2% in 2026-27, before declining in the final two years of the forecast to 92.8% in 2028-29.

£27BN FISCAL WINDFALL

According to the OBR, the Chancellor had financial headroom of around £27bn, almost all of which he spent in three areas: a 2% cut in NICs, permanent tax relief for business investment, and further welfare reforms, “leaving debt falling by a narrow margin in five years”. The report continued:

“Higher inflation boosts tax revenues but also welfare benefits while higher interest rates push up debt servicing. But because departmental spending is left largely unchanged, this delivers a net fiscal windfall of £27bn.”

INTEREST RATES TO 2029

Following a series of 14 consecutive base rate hikes, the BoE maintained its base rate at 5.25% for the first time in nearly two years this September. The rate also remained unchanged in November, with the next monetary policy decision expected on 14 December.

The sharp fall in inflation does not yet mean the BoE is ready to start reducing interest rates.

Indeed, according to BoE governor, Andrew Bailey, more rate rises could be on the cards, saying it is “far too early to be thinking about rate cuts”. The OBR confirmed that markets expected the Bank Rate to peak at “only a little above” the current 5.25% in the final quarter of the year, before falling back to 4% by 2029.